Endings and beginnings: Year-end tax reminders and tax changes in 2023

“Celebrate endings – for they precede new beginnings.”

— Jonathan Lockwood Huie

Here we are with two days left in 2022! For the past few weeks, most of us have been busy giving gifts and ticking off grocery lists as we finish our last-minute preparations for media noche, and coming up with resolutions for the new year. As we celebrate this ho-ho-holiday season with our loved ones and look forward to a new year full of new hopes, goals, and beginnings, let’s also make sure we tick off our year-end tax checklist.

Here are a few guidelines to help you make your personalized tax checklist.

CORPORATE INCOME TAX (CIT) FILINGS

For corporate taxpayers following a calendar year, the deadline for filing of the 2022 annual corporate income tax returns (ITRs) is April 17, 2023. The submission of the required attachments to the ITR is also due on the same date for manual filers, and on May 2 for both eBIR and eFPS filers.

Meanwhile, for PEZA and BoI-registered business enterprises, the submission of the duly filed ITR and Audited Financial Statements (AFS) is due on May 17, 2023.

For companies with a fiscal year end other than Dec. 31, the deadline for filing the annual ITR is on the 15th day of the fourth month following the close of the fiscal year. This also applies for the deadline of submission of the required attachments to the filed ITR for manual filers. For eBIR and eFPS filers, on the other hand, the deadline is within 15 days from the statutory due date or date of filing/payment of the ITR, whichever is later. The submission of the filed ITR and AFS to PEZA and the BOI must be within 30 days from the statutory due date or date of filing/payment of the ITR, whichever comes later.

It is also worth noting that certain taxpayers are required to enroll in eFPS or use the eBIRForms Package to electronically file their ITRs. Taxpayers who are required to file electronically but file and pay manually may be liable for “wrong venue” filing.

ATTACHMENTS TO THE ANNUAL ITR

Revenue Memorandum Circular (RMC) No. 28-2022 provides a list of required attachments for annual submission of the ITR. Following RMC No. 46-2021, all tax returns, attachments, and documents identified under RMC No. 28-2022 can be signed by the taxpayer or authorized officer or signatory using an electronic signature (e-signature). Such e-signature is deemed equivalent to an actual or “wet” signature for filing purposes.

These attachments may be submitted to the BIR manually or through the eAFS platform.

OTHER CIT-RELATED MATTERS

The Minimum Corporate Income Tax (MCIT) rate of 1% under Section 27(E) of the Tax Code, as amended by the CREATE Law will still be in effect for CY2022. Note, however, that the Net Operating Loss Carry-Over (NOLCO) incurred in CY2022 can only be carried over as a deduction from gross income for the next three consecutive taxable years. The extension to five years is no longer applicable.

In case there’s an overpayment of income tax, ensure that the preferred recovery method is ticked correctly in the ITR, as, unlike our many new year’s resolutions, this is irrevocable.

WHAT LIES AHEAD FOR 2023?

For 2023, here’s a quick list of changes affecting tax compliance, most of which are good tidings.

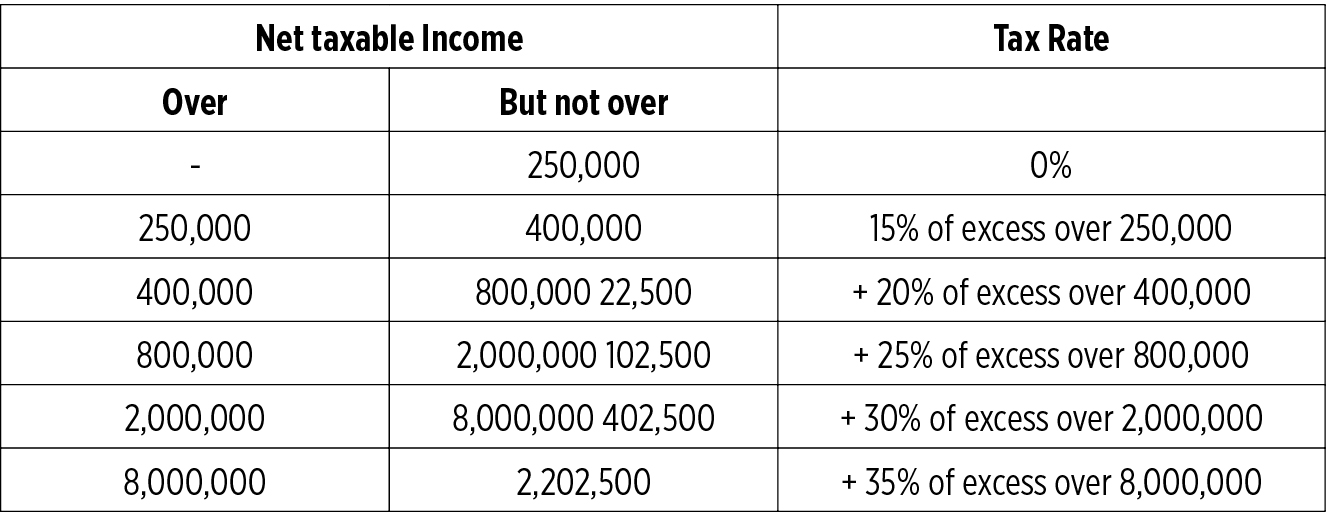

Lowered tax rates for individual taxpayers

Effective Jan. 1, there will be a reduction in the graduated income tax rates for individual taxpayers, as presented in the table.

Reduced frequency of VAT filings

Starting Jan. 1, taxpayers will only be required to file four quarterly Value-Added Tax (VAT) returns instead of 12 filings per taxable year.

Reversion of the previously lowered tax rates

Effective July 1, the following taxes, which were previously lowered, will revert to their original rates: Minimum Corporate Income Tax from 1% to 2%; Percentage Tax for non-VAT taxpayers from 1% to 3%; and Special Income Tax Rate for Non-Profit Proprietary Educational Institutions and Hospitals from 1% to 10%.

Increase in mandatory government contributions

There will be an increase in Philhealth and Social Security System (SSS) contributions effective 2023. The Philhealth premium rate will increase from 4% to 4.5%, while the SSS contributions will increase from 13% to 14% — the employer’s share in an employee’s SSS contribution will rise from 8.5% to 9.5%.

The above reminders should help you kick-start your own year-end tax compliance checklist — and like Santa Claus, don’t forget to check it twice (or even thrice!). We need to ensure we’re not naughty, but nice and responsible taxpayers.

The views or opinions expressed in this article are solely those of the author and do not necessarily represent those of Isla Lipana & Co. The content is for general information purposes only, and should not be used as a substitute for specific advice.

Aubrey Gayle T. Diaz is an Assistant Manager at the Tax Services Department of Isla Lipana & Co., the Philippine member firm of the PwC network.